With the financial year closing, reports like Inc42,IVCA, Bain and Co threw some light into how Covid impacted the startup ecosystem last year. Here are some of the key findings:

-

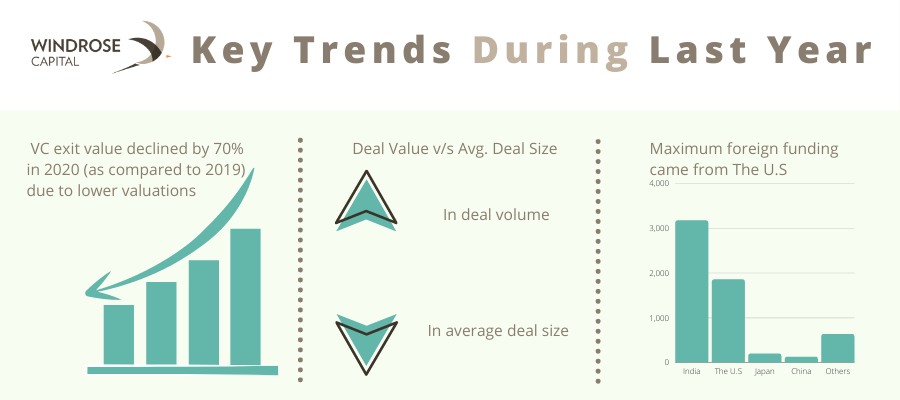

Key trends of COVID

There was a significant increase in the incoming volume of deals, but the average deal size decreased. Which meant that there were more startups seeking funds in the last year. However, the average cheque sizes tended to be lesser than the previous years. $17M was the average ticket size in 2020.

There was a strong incoming deal flow especially from sectors like Consumer Tech and SaaS. This also implied a strong growth in the startups with many focusing on expanding to different regions. Though over 15% of the startups were forced to shut, many chose to halt their operations and pick up the pace later on during the year. Few of our portfolio entities even expanded globally while some strengthened their presence locally.

A slowdown in Exits was also a key trend. Many prominent startups thought it wise to put their exit plans on hold. VCs and investors too thought of assisting their portfolio companies further and not focusing on the exits for the next few years. In fact, bridge stage fundings reached a historic peak last year.

Fundraising was at an all-time high with even foreign investors coming into the picture. The US was generally seen leading the way in funding the maximum number of ventures as well as contributing to the largest amount of funds.

-

Sectors in focus

TLDR: Investments in consumer tech, SAAS and fintech accounted for 75% of VC investments in 2020. Key sub-sectors receiving investments included (a) ed-tech, food-tech, gaming, and media and entertainment in consumer tech; (b) verticalized solutions within SaaS; and (c) payments within fintech.

A generalized trend is that if the 2010s saw startups concentrating on the bigger picture, the 2020s is all about breaking the bigger picture down and targeting the niches exclusively. This saw a huge trend with many startups hyper localizing and focusing on ‘local’ outlets (pharmacies, eateries, kirana stores etc) that could find tech adoption useful in expanding their business.

However, many sectors grew amid the lockdown because of the lockdown. Ed-tech definitely stole the spotlight, with the tremendous growth and offerings they provided to their audience. Many key acquisitions also happened in the sector such as Aakash and WhiteHat Jr’s acquisition by Byju’s which also saw valuations of the industry as a whole soar sky-high. After the sector gained significant traction in the early days of the lockdown, many new startups emerged offering differentiated services like ed-tech in vernacular languages or niche vocations. It’ll be interesting to see the sector innovating post the lockdown to co-exist with regular classes/tuitions.

Food-tech was also a prominent sector that emerged during the lockdown. It was also considered a 'life-saver by many during the lockdown.

Gaming, media and entertainment also saw a big rise. In these sectors, many new startups were born during the first few months of the lockdown. And many raised funds during the last quarter of the year. There was a surge in investing activities of these companies, especially in the early stages.

However, the largest number of active startups were found in the enterprise tech field. B2B enterprise is a powerful space to be in right now, especially considering the rise of the B2B marketplace over the past few years. Our investment thesis at Windrose Capital is very encouraging of this sector as a whole, as we see significant value creation in this space in the upcoming years. Evidently, the enterprise sector is also the most funded sector at the seed stage.

.png)

-

What's Next?

With the ongoing second wave in India, it becomes harder to speculate what trends will dominate the ecosystem next. However, these reports do give fair insights into what has worked so far.

In total, 22 start-ups raised over $100 million in 2020 from VC and growth equity investors, with the majority concentrated in consumer tech.

There are few verticals to watch out for in the Fintech sector, as more retail investors are seeking ways to invest. Lending and Wealth-management sectors enjoyed popularity last year. In the upcoming years, trends like payments, wealth management, insurtech, and lending are bound to rise.

SaaS clearly saw signs of maturity, and perhaps this is here to stay. Vertical SaaS saw a rise in funding as compared to previous years. However, in the upcoming years, experts see a rise in the board based horizontal and vertical solutions serving enterprises and SMBs.

*All the data points here are derived from Inc42 and IVCA's reports.